Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026? : Personal Loan vs Payday Loan comparison for 2026. Learn differences, interest rates, risks, and which option is safer for your financial needs.

Table of Contents

Introduction

Money problems rarely come with a warning. One day everything feels stable, and the next, you’re searching for quick cash options. That’s where the debate around Personal Loan vs Payday Loan starts to matter.

If you’ve ever been stuck between these two choices, you’re not alone. Both promise fast access to funds, but they work very differently—and the consequences can be drastically different too.

In this guide, we’ll break down Personal Loan vs Payday Loan in a practical, no-nonsense way. By the end, you’ll know exactly which option fits your situation in 2026—and which one you should probably avoid.

What Is a Personal Loan?

A personal loan is a type of unsecured loan offered by banks, credit unions, and online lenders. You borrow a fixed amount and repay it over time in monthly installments : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

Key Features:

- Fixed interest rates (in most cases)

- Repayment period: 1 to 5 years

- Higher loan amounts

- Requires a credit check

Personal loans are commonly used for: Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

- Medical expenses

- Debt consolidation

- Home repairs

- Emergency costs

What Is a Payday Loan?

A payday loan is a short-term, high-interest loan meant to cover urgent expenses until your next paycheck : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

Key Features:

- Very short repayment period (usually 2–4 weeks)

- Extremely high interest rates

- Minimal or no credit check

- Small loan amounts

They are often marketed as “quick cash” solutions, but they come with serious risks.

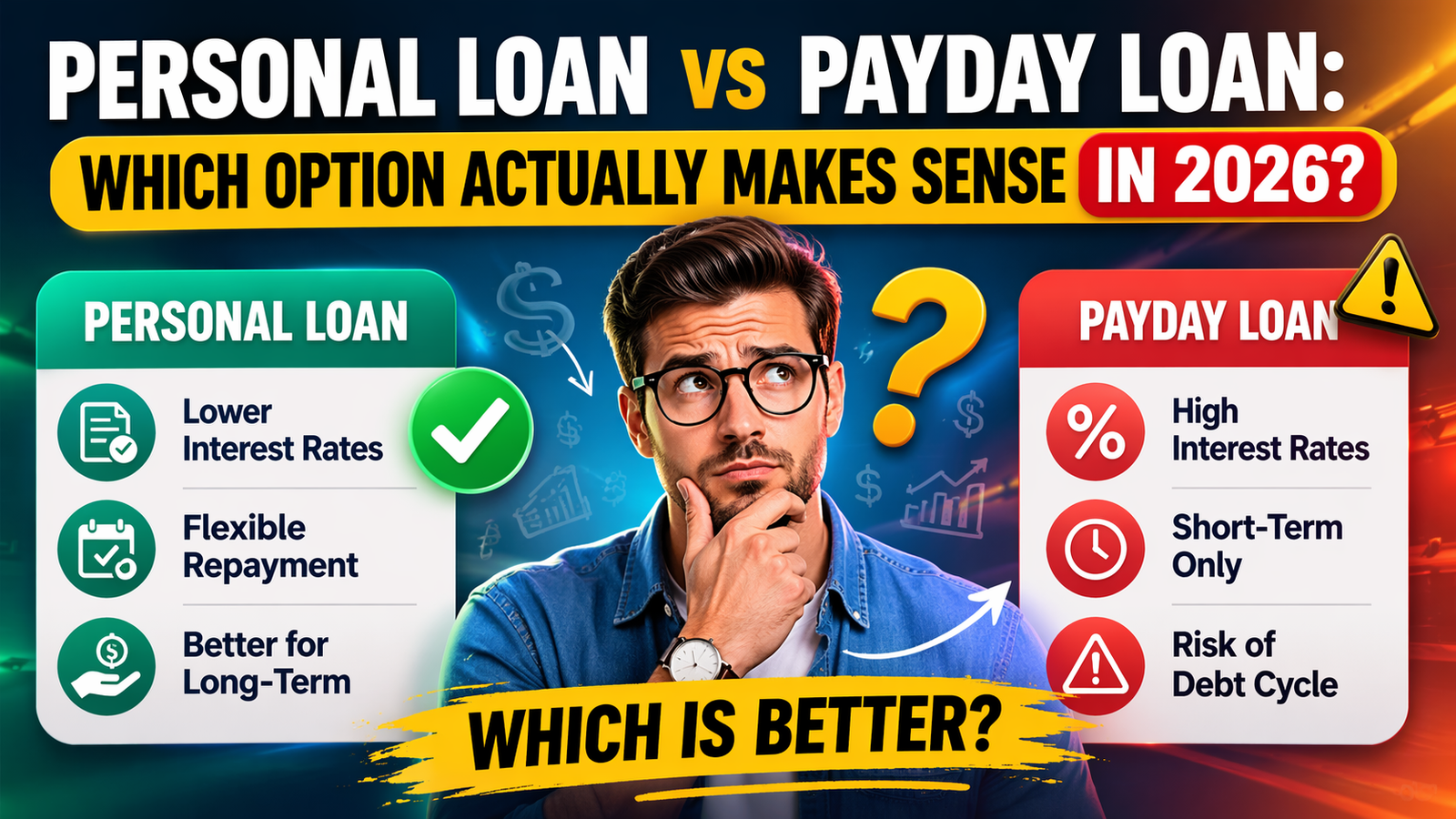

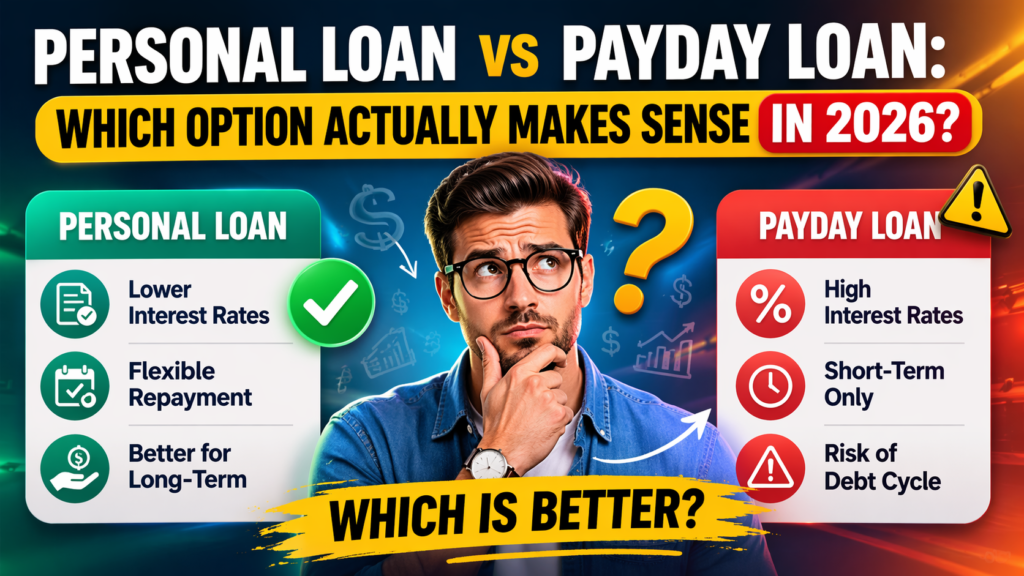

Personal Loan vs Payday Loan: Core Differences

Let’s get straight to the point. Here’s how Personal Loan vs Payday Loan compares across key factors: Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

1. Interest Rates

- Personal Loan: 10% – 25% annually

- Payday Loan: Can exceed 300% annually

This alone makes a huge difference. In the Personal Loan vs Payday Loan comparison, payday loans are significantly more expensive.

2. Repayment Terms

- Personal Loan: Flexible monthly payments over years

- Payday Loan: Full repayment in a few weeks

With Personal Loan vs Payday Loan, repayment pressure is much higher with payday loans.

3. Loan Amount

- Personal Loan: Higher borrowing limits

- Payday Loan: Usually small amounts

If you need substantial funds, the Personal Loan vs Payday Loan choice becomes obvious—personal loans offer more flexibility.

4. Approval Process

- Personal Loan: Requires credit check

- Payday Loan: Easy approval, minimal checks

This is one area where payday loans seem attractive. But ease of approval often comes at a cost : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

5. Risk Level

- Personal Loan: Lower risk if managed well

- Payday Loan: High risk of debt cycle

In any honest Personal Loan vs Payday Loan discussion, risk is a critical factor.

When a Personal Loan Makes Sense

There are situations where choosing a personal loan is the smarter financial move : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

Ideal Scenarios:

- You have a stable income

- You need a larger amount

- You can manage monthly payments

- You want predictable costs

In the Personal Loan vs Payday Loan debate, personal loans win when you’re thinking long-term.

When a Payday Loan Might Be Considered

Let’s be realistic—payday loans exist for a reason : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

Possible Use Cases:

- Emergency cash needed immediately

- No access to traditional credit

- Very small amount required

- Short-term repayment certainty

Even then, the Personal Loan vs Payday Loan comparison suggests caution. Payday loans should be a last resort, not a regular solution.

Hidden Costs You Should Know

One of the biggest mistakes people make in the Personal Loan vs Payday Loan decision is ignoring hidden costs : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

Personal Loan Costs:

- Processing fees

- Late payment penalties

Payday Loan Costs:

- Extremely high fees

- Rollover charges

- Penalties that compound quickly

Payday loans often look simple upfront but become expensive fast.

Debt Trap Risk: The Real Problem

Here’s where things get serious : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

With payday loans, many borrowers can’t repay on time. So they take another loan to cover the first one. This creates a cycle.

In the Personal Loan vs Payday Loan comparison, this is the biggest red flag.

Personal loans, while not risk-free, are structured to avoid this trap—if used responsibly.

Impact on Credit Score

Personal Loan:

- Helps build credit history

- Improves score with timely payments

Payday Loan:

- Often doesn’t improve credit

- Can damage score if unpaid

So in the Personal Loan vs Payday Loan discussion, personal loans clearly support long-term financial health.

Real-Life Example

Let’s say you borrow $1,000.

Personal Loan:

- Interest: ~12% annually

- Repayment: 12 months

- Total cost: manageable

Payday Loan:

- Fee: $15 per $100

- Total fee: $150 in weeks

Now imagine rolling it over multiple times. The cost skyrockets.

This is why Personal Loan vs Payday Loan isn’t just a choice—it’s a financial decision that can impact your future : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

Safer Alternatives to Consider

Before choosing either option, consider these: Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

- Credit union loans

- Borrowing from family

- Employer salary advances

- 0% APR credit cards

Even in the Personal Loan vs Payday Loan comparison, alternatives can sometimes be better than both.

Pros and Cons Summary

Personal Loan

Pros:

- Lower interest rates

- Predictable payments

- Builds credit

Cons:

- Requires good credit

- Slower approval

Payday Loan

Pros:

- Fast approval

- Easy access

Cons:

- Extremely high cost

- High risk of debt trap

Final Verdict: Personal Loan vs Payday Loan

So, which one is better?

In most cases, Personal Loan vs Payday Loan is not even a close contest. Personal loans are safer, cheaper, and more sustainable.

Payday loans might solve a short-term problem, but they often create a bigger one.

Conclusion

Choosing between Personal Loan vs Payday Loan comes down to more than speed—it’s about long-term impact. While payday loans offer quick relief, they can quickly spiral into costly debt.

Personal loans, on the other hand, provide structure, transparency, and a path toward better financial stability.

If you’re in a tough spot, take a moment before deciding. Look at the numbers. Think beyond the immediate need. In the Personal Loan vs Payday Loan decision, the smarter choice is usually the one that protects your future—not just your present : Personal Loan vs Payday Loan: Which Option Actually Makes Sense in 2026?

FAQ Section

1. What is the main difference between personal loan and payday loan?

A personal loan is repaid over months or years with lower interest, while a payday loan must be repaid quickly with very high fees.

2. Is a payday loan ever a good idea?

Only in extreme emergencies when no other option is available—and even then, it should be used cautiously.

3. Does a personal loan affect credit score?

Yes, positively if you make timely payments. It can help build your credit history.

4. Why are payday loans considered risky?

Because of high interest rates and the possibility of falling into a debt cycle due to short repayment periods.

5. Which is cheaper: personal loan or payday loan?

In almost all cases, a personal loan is significantly cheaper than a payday loan.

6. Can I switch from payday loan to personal loan?

Yes, many people use personal loans to consolidate and pay off payday loan debt more safely.